|

Investment Options ╗ Private Lending

|

Are you consistently earning more than 10% with your current investments?

If not, you want to seriously consider being a private lender.

Invest in safe, short-term, secured loans at 10-14%.

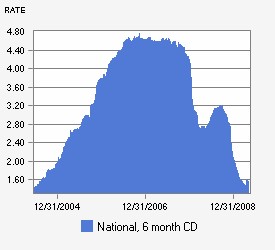

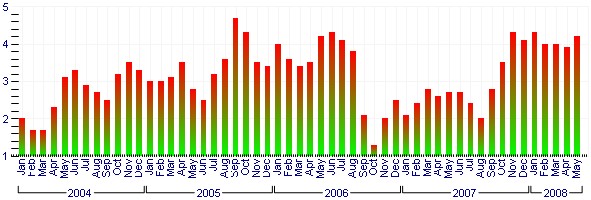

The conventional, ōsafeö investment vehicles are certificates of deposit (CDs) and maybe mutual funds because of their diversification and knowledgeable fund managers. For years now, CD rates have been below 5%. On average, a 4% return has been a good rate for CDs. See the graph below for CD rates over the last 5 years. Notice that since 2009 it has been hard to get a rate over 2 percent.

CD Rates over The Last 5 Years

The most troubling concern when investing in CDs is the rate of inflation. If the rate of inflation is higher than your rate of return on your CD, which it often is, the purchasing power of your assets is actually decreasing! Notice how the annual inflation rate also ranges from 1.5% to 5% over the last few years.

ANNUAL INFLATION RATES FROM 2004 THROUGH EARLY 2008

So, if you are getting a 3% return on your money, but the cost of goods increased by over 3%, your purchasing power decreased! You canÆt buy a nicer car or send your kid to a nicer college or travel more when you retire. Your wealth did not increase. You can not purchase the same quality or quantity of goods or services as when you invested in the CD.

What about mutual funds. Some more aggressive mutual funds can get returns better than 10% for a period of time, but over many years they rarely return over 10%, and many times you actually lose money in a mutual fund (i.e. a loss or a negative rate of return!). Mutual funds also do better in a bull market because of limitations on trading strategies for fund managers. So when the market drops, your investment is likely to drop too. And with a struggling economy and ōbaby boomersö pulling money out of mutual funds in retirement accounts for retirement, the market is likely to keep dropping, along with the value of your investment. Of course, in 2008 the market dropped to its lowest value in over 10 years.

Stock Market Trends Over the last 10 Years

So since early 2009, CDs are giving returns below 2% and most people took heavy losses with their mutual funds.

Maybe it is a good time to start getting a better return on your money. Our private lenders are currently getting 14% return on their six month investments.

The graph below demonstrates the powerful effect of getting an increased return on your money. Just increasing your return from 4% to 14% can help you increase your interest income considerably!

|

| |

14% Rate of Return |

4% Rate of Return |

| Year |

Total |

Interest |

% Growth |

Total |

Interest |

% Growth |

| 0 |

$100,000 |

$14,000 |

|

$100,000 |

$4,000 |

|

| 1 |

$114,000 |

$15,960.00 |

14% |

$104,000 |

$4,160 |

4% |

| 2 |

$129,960 |

$18,194 |

30% |

$108,160 |

$4,326 |

8% |

| 3 |

$148,154 |

$20,741 |

48% |

$112,486 |

$4,499 |

12% |

| 4 |

$168,896 |

$23,645 |

69% |

$116,986 |

$4,479 |

17% |

| 5 |

$192,541 |

$26,956 |

93% |

$121,665 |

$4,867 |

22% |

| 6 |

$219,497 |

$30,729 |

119% |

$126,531 |

$5,061 |

27% |

| 7 |

$250,227 |

$35,032 |

150% |

$131,593 |

$5,264 |

32% |

| 8 |

$285,259 |

$39,936 |

185% |

$136,857 |

$5,474 |

37% |

| 9 |

$925,195 |

$45,527 |

225% |

$142,331 |

$5,693 |

42% |

| 10 |

$370,722 |

$51,901 |

271% |

$148,024 |

$5,921 |

48% |

| 11 |

$422,623 |

$59,167 |

323% |

$153,945 |

$6,158 |

54% |

| 12 |

$481,790 |

$67,451 |

382% |

$160,103 |

$6,404 |

60% |

| 13 |

$549,241 |

$76,894 |

449% |

$166,507 |

$6,660 |

67% |

| 14 |

$626,135 |

$87,659 |

526% |

$173,168 |

$6,927 |

73% |

| 15 |

$713,794 |

$99,931 |

614% |

$180,094 |

$7,204 |

80% |

| 16 |

$813,725 |

$113,921 |

714% |

$187,298 |

$7,492 |

87% |

| 17 |

$927,646 |

$129,871 |

828% |

$194,790 |

$7,792 |

95% |

| 18 |

$1,057,517 |

$148,052 |

958% |

$202,582 |

$8,103 |

103% |

| 19 |

$1,205,269 |

$168,780 |

1,106% |

$210,685 |

$8,427 |

111% |

| 20 |

$1,374,349 |

$192,409 |

1,274% |

$219,112 |

$8,764 |

119% |

|

|

The table demonstrates that it would take 18 years to double your money at 4% or less than six years at 14%. After 18 years, the $100,000 investment increased almost ten-fold to over one million dollars. This is the power of compounded interest at a reasonable rate.

So take control of your money invested in your IRA, Pension Plan, Savings or CDs.

Contact us today with your investment potential.

Another possibility is unlocking some of the equity in your home and using it to make good returns. There are plenty of refinance or home equity lines of credit (HELOCs) loans available today at under 7% APR. You could take out $200,000 and invest it at twice the rate (14%) to gain a net 7% on unused money. This would give you an extra $14,000 per year or an extra $1167 per month, plus you gain the tax benefit of writing off the interest payments on the home loan.

If this interests you, we can assist you through the entire process to unlock the equity in your home and turn it into an additional monthly income. Contact us today for a free consultation to find out how we can help you make a few extra thousand dollars a month by unlocking all that equity in your home.

|

©2006-2009 Roberti Real Estate. All Rights Reserved.

Terms Of Use | Privacy Policy | Site Map |

|